BROOKLYN NEW DEVELOPMENT MARKET REPORT

BROOKLYN NEW DEVELOPMENT MARKET REPORT ARCHIVE

sign up for Sponsor Sale reports to be sent to your email

TABLE OF CONTENTS

JUMP TO A PARTICULAR SECTION

INTRODUCTION

MNS IS PROUD TO PRESENT THE SECOND QUARTER 2024 EDITION OF OUR NEW DEVELOPMENT MARKET REPORT.

New Development Sales data, defined as “Arms-Length” first offering transactions where the seller is considered a “Sponsor”, was compiled from the Automated City Register Information System (ACRIS) for sponsor sales that traded during the Second Quarter of 2024 (4/1/24– 6/30/24). All data is summarized on a median basis.

MARKET SNAPSHOT

15.3%

YEAR-OVER-YEAR

MEDIAN PPSF

3.8%

QUARTER-OVER-QUARTER

MEDIAN PPSF

26.5%

YEAR-OVER-YEAR

MEDIAN SALES PRICE

5.7%

QUARTER-OVER-QUARTER

MEDIAN SALES PRICE

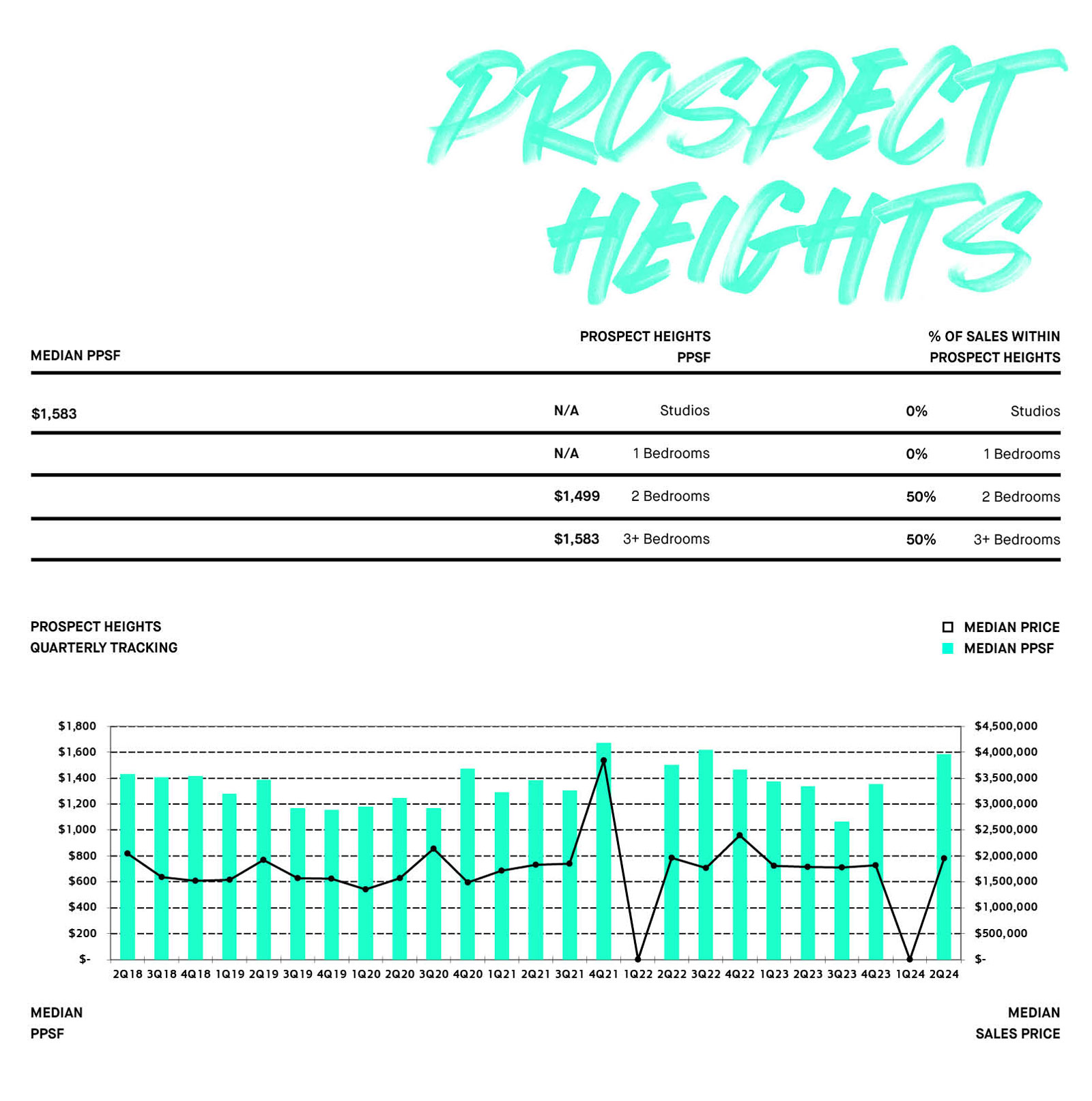

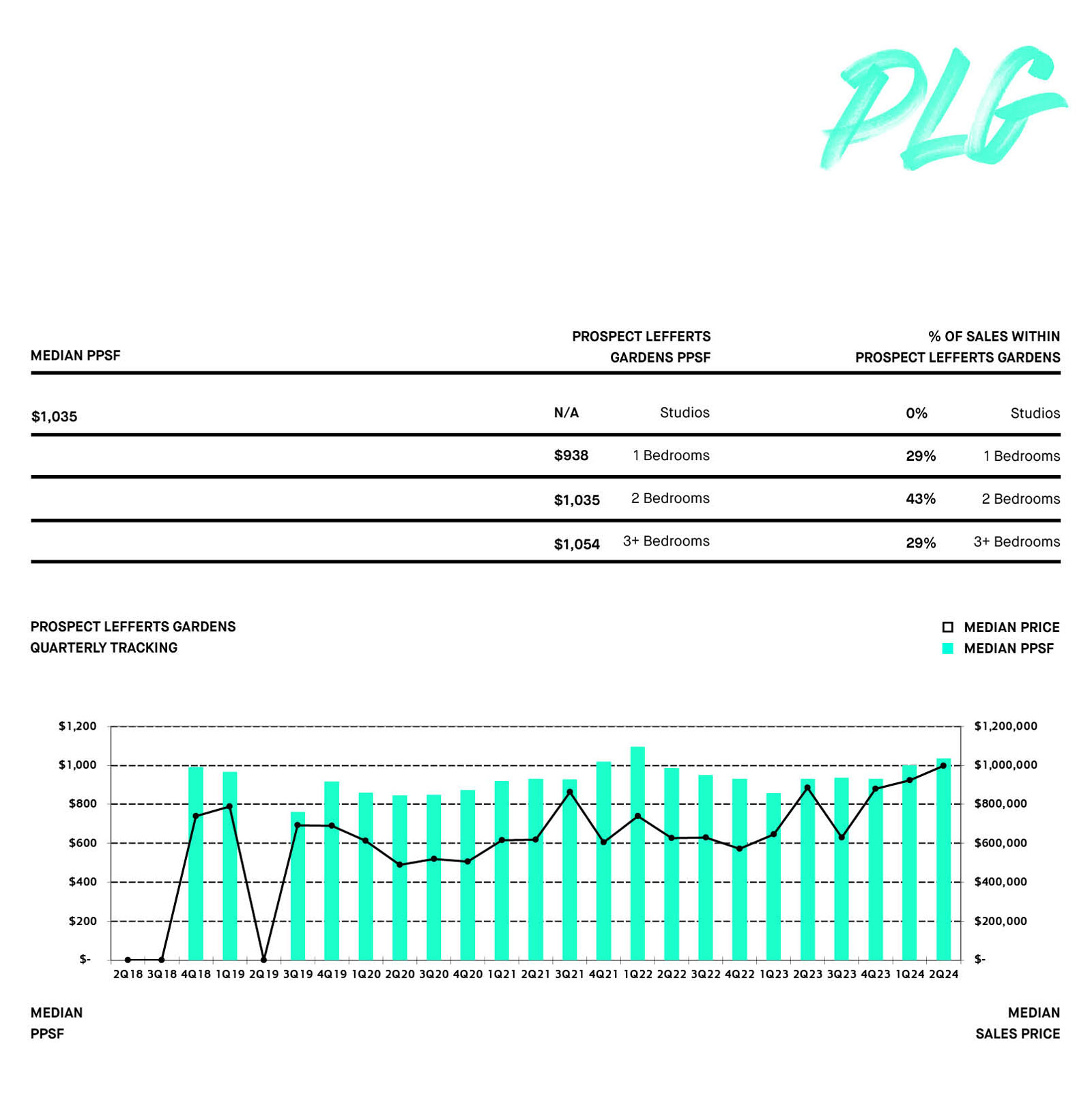

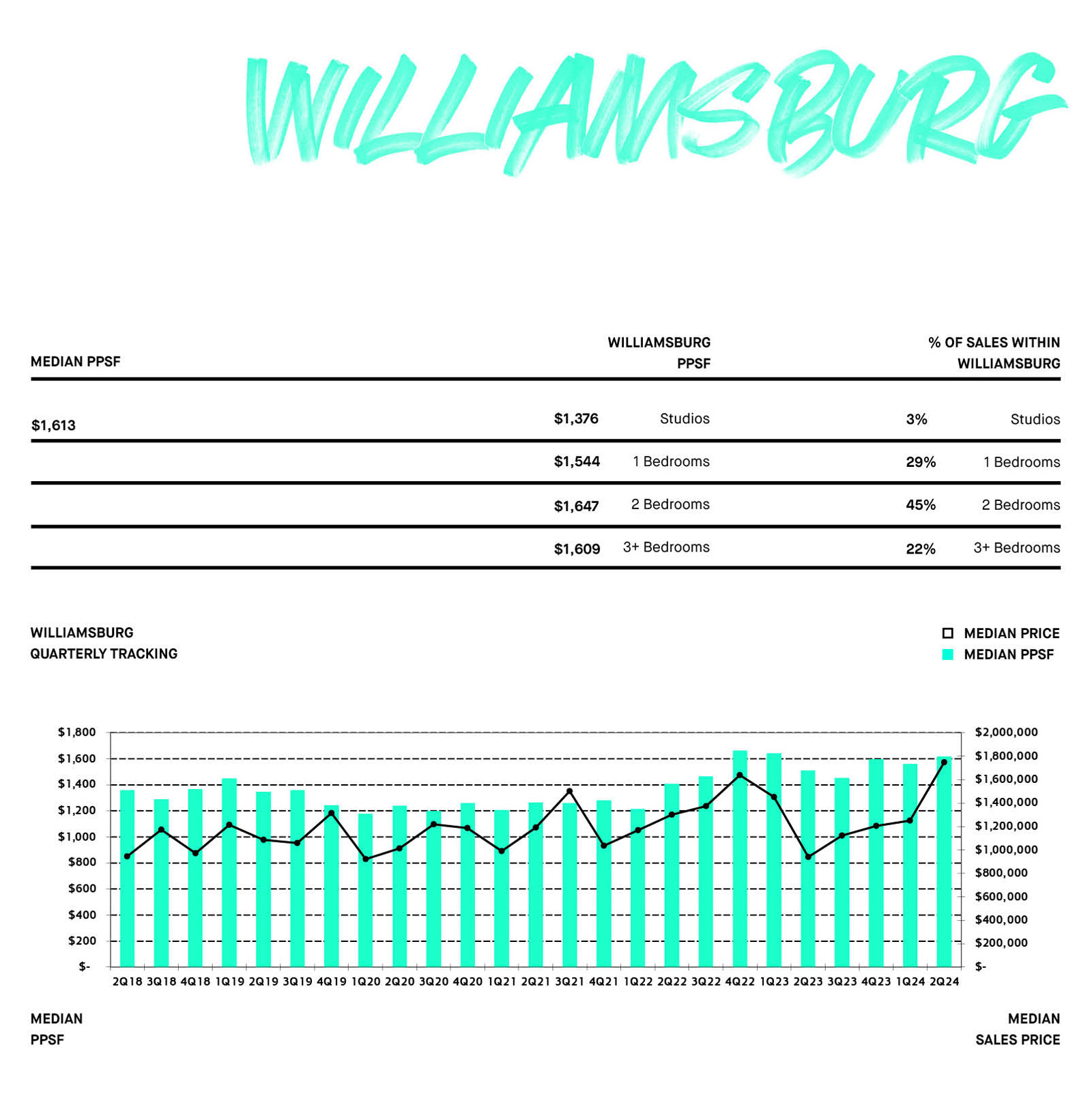

BROOKLYN NEW DEVELOPMENT SPONSOR SALES

NEIGHBORHOOD WITH THE MOST NEW DEV SALES

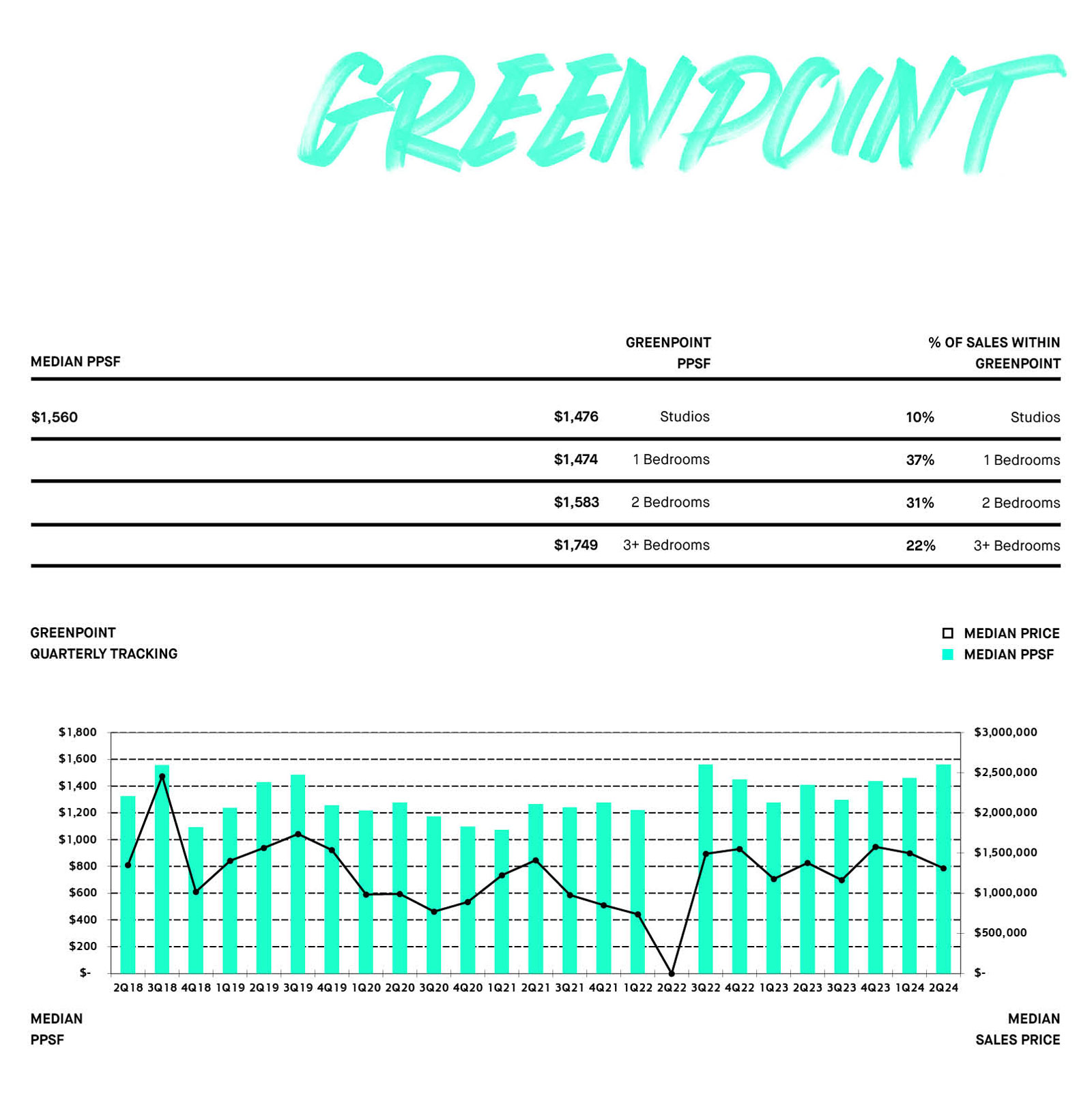

GREENPOINT

26.0% of Brooklyn New Dev Sales

TOTAL NEW DEVELOPMENT SALES VOLUME

$491,217,935 in 1Q24

LARGEST QUARTERLY UP-SWING

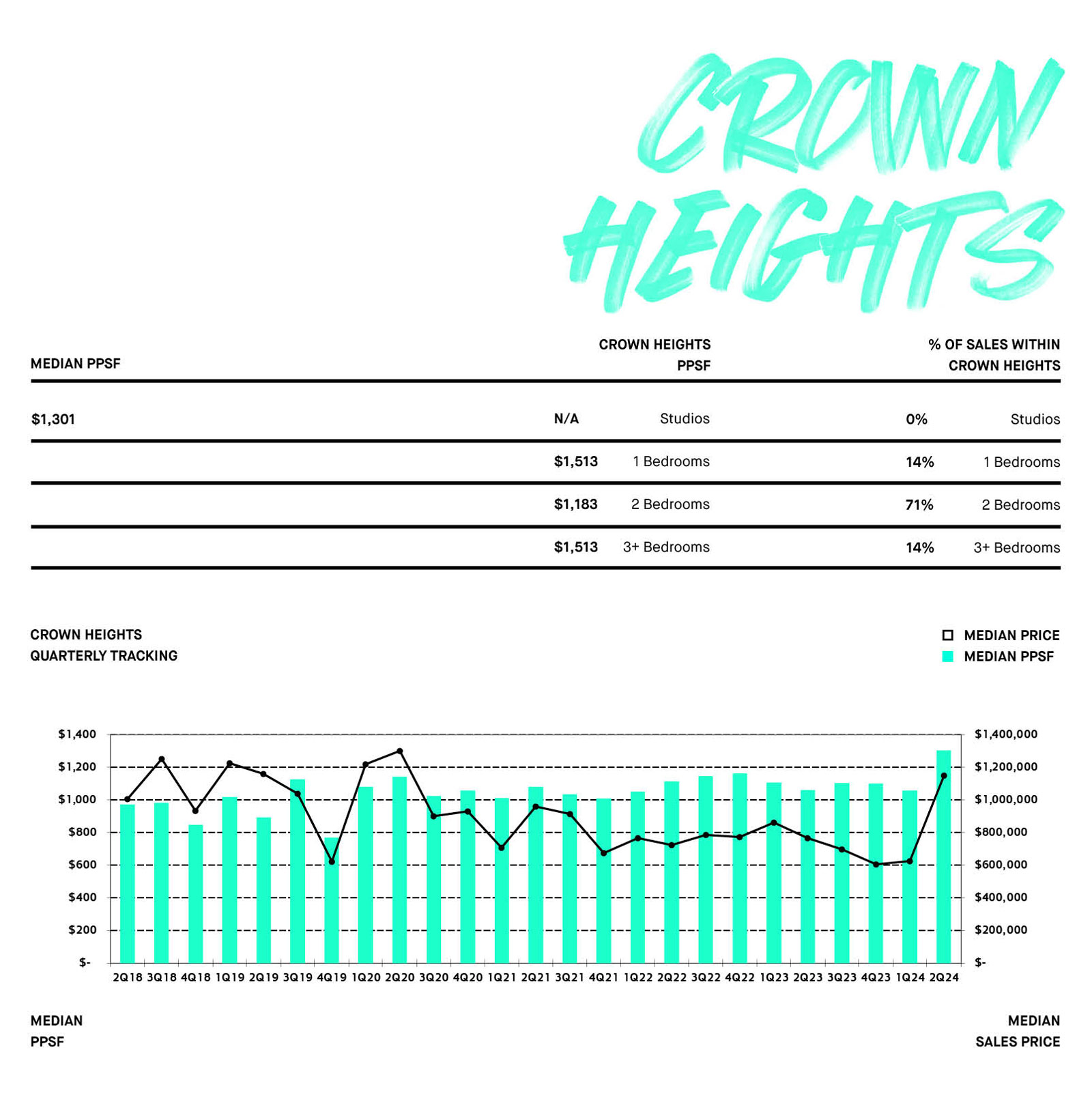

CROWN HEIGHTS

PPSF $1,301/SF from $1,054/SF

Sales Price $1,150,000 from $625,000

LARGEST QUARTERLY DOWN-SWING

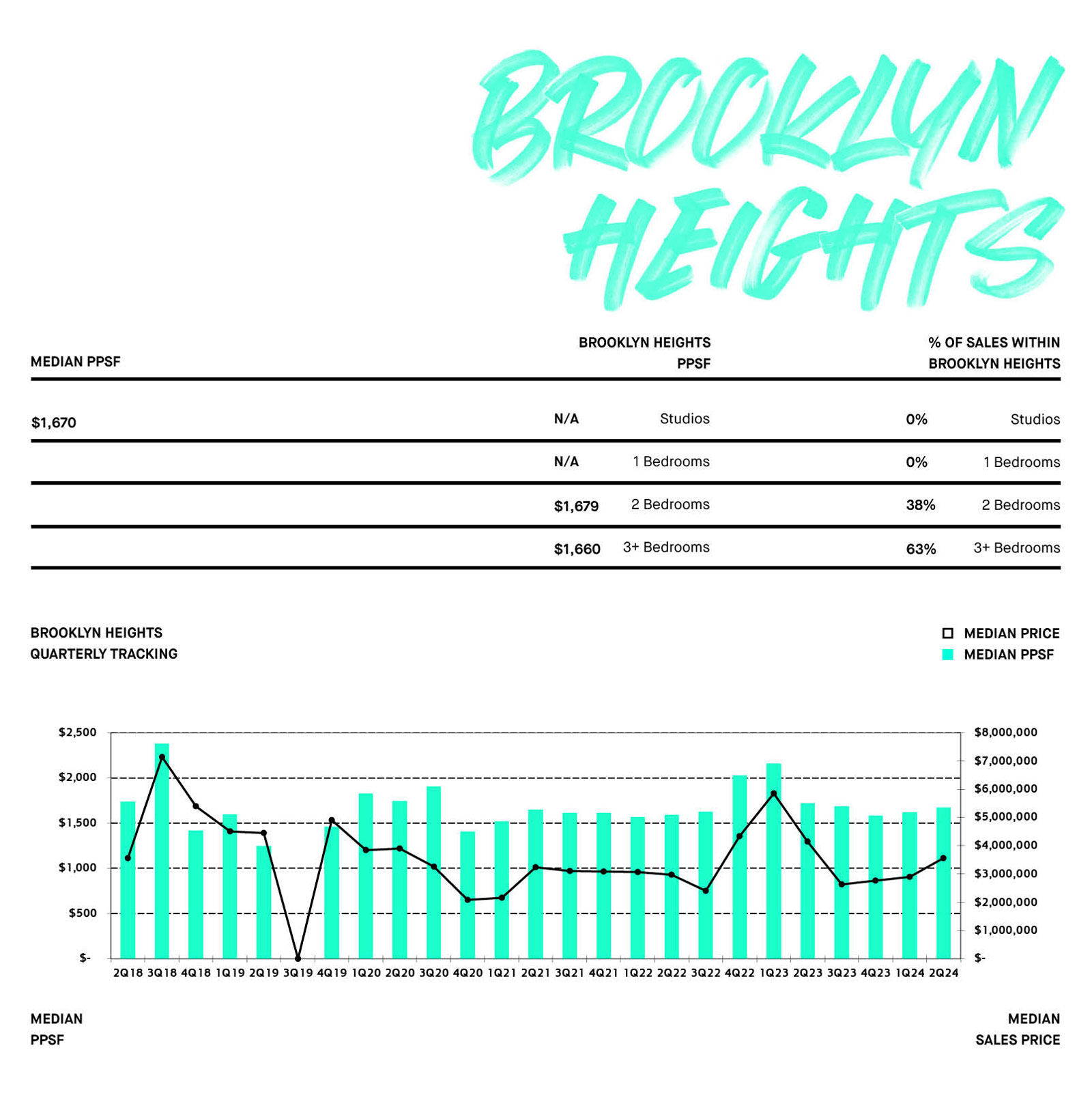

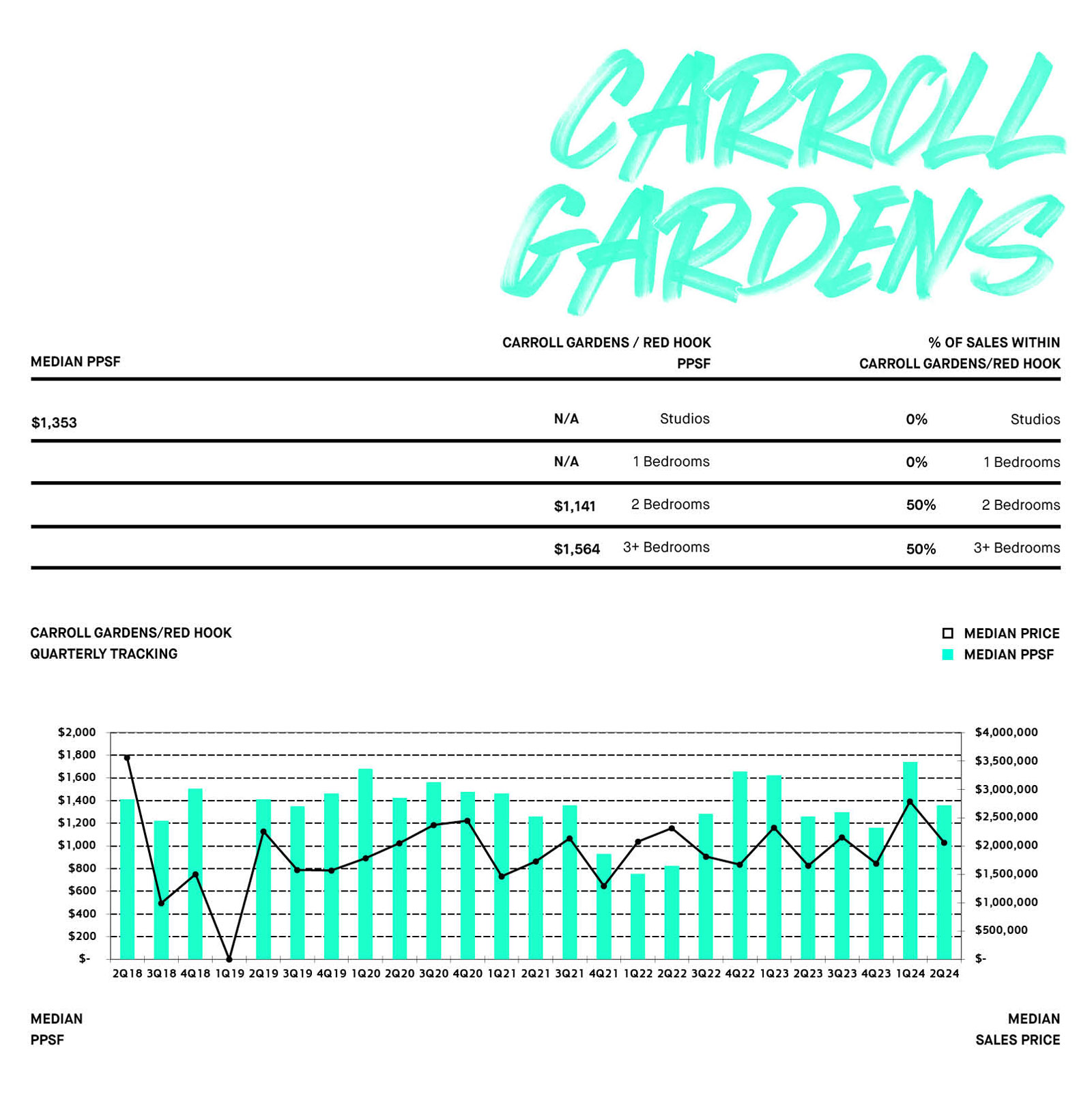

CARROLL GARDENS / RED HOOK

PPSF $1,353 from $1,739

Sales Price $2,060,000 from $2,785,000

HIGHEST NEW DEVELOPMENT SALE PPSF

60 FRONT STREET 26B $2,524 PPSF

HIGHEST NEW DEVELOPMENT SALE

60 FRONT STREET 26B $6,700,000

MARKET SNAPSHOT

MARKET SUMMARY

Quarter-over-quarter, total new development sales volume in Brooklyn increased by 18.46%, from $491,217,935 in 1Q24 to $581,898,737 in 2Q24, and the

total number of sponsor sales increased by 12.90% from 341 to 385. Quarter-over-quarter, the median price per square foot for increased by 3.8%, from

$1,392 to $1,445 as the median sales price paid increased by 5.7%, from $1,195,000 to $1,262,547. Year-over-year, median price per square foot increased

by 15.3%, from $ 1,253 to $1,445 psf, and the median sales price increased by 26.5%, from $997,885 to $1,262,547.

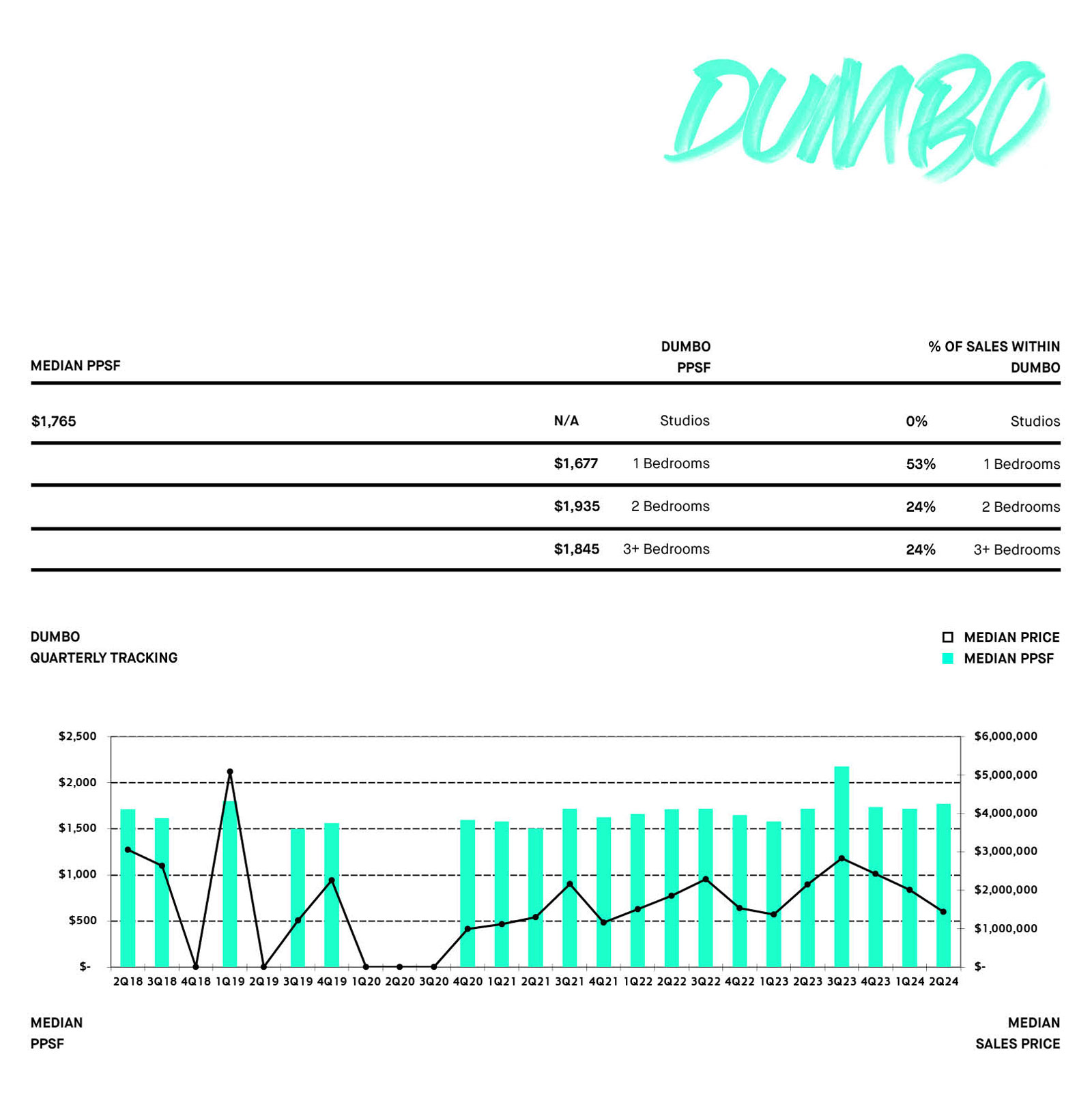

This past quarter, the highest sales price and the highest price per square foot paid both occurred at Olympia on 60 Front Street in DUMBO where unit 26B

sold for $6,700,000 ($2,524 psf).

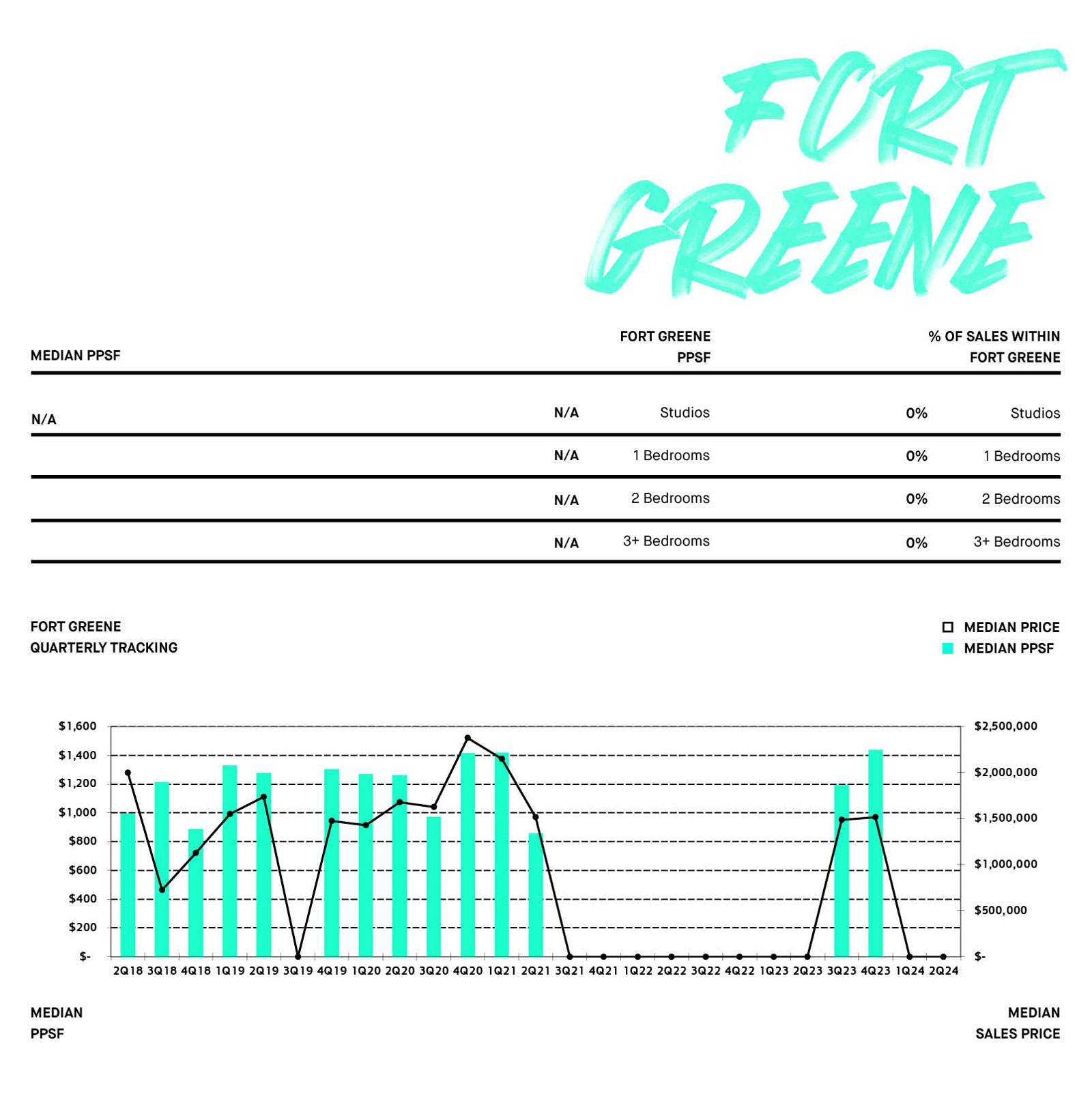

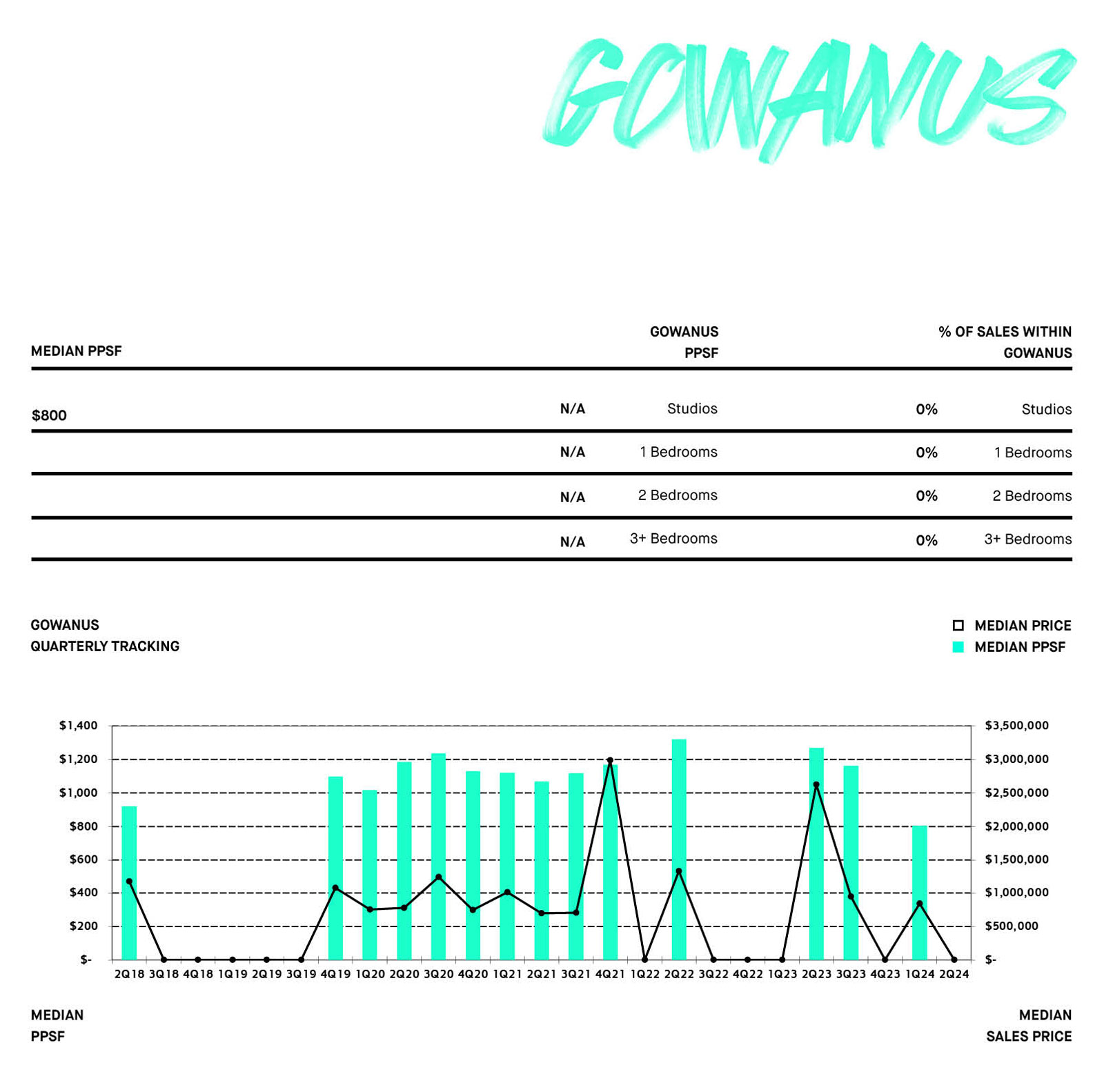

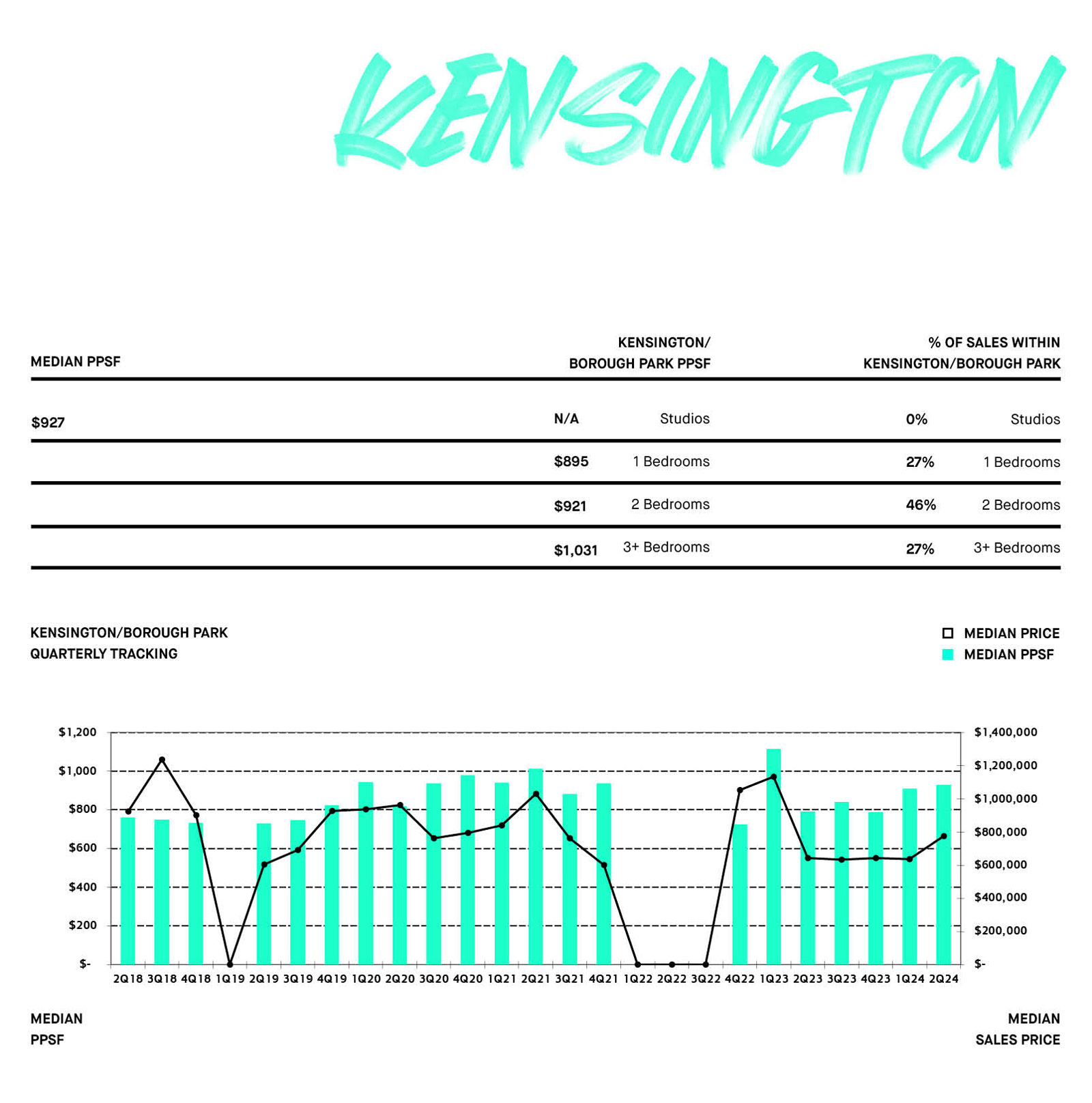

Greenpoint saw the largest percentage of Brooklyn Sponsor Sales closings this quarter at 25.97%, or 100 out of the 385 total closings.

MARKET UP-SWINGS

The largest quarterly up-swing by price per square foot occurred in Crown Heights, which increased by 23.5% from $1,054 psf to $1,301 psf, as the median sales price increased by 84.0%, from $625,000 to $1,150,000.

MARKET DOWN-SWINGS

The largest down-swing this quarter occurred in Carroll Gardens / Red Hook, where the median price per square foot decreased by 22.2%, from $1,739 psf to $1,353 psf, as the median sales price decreased by 26.0%, from $2,785,000 to $2,060,000.

MARKET TRENDS

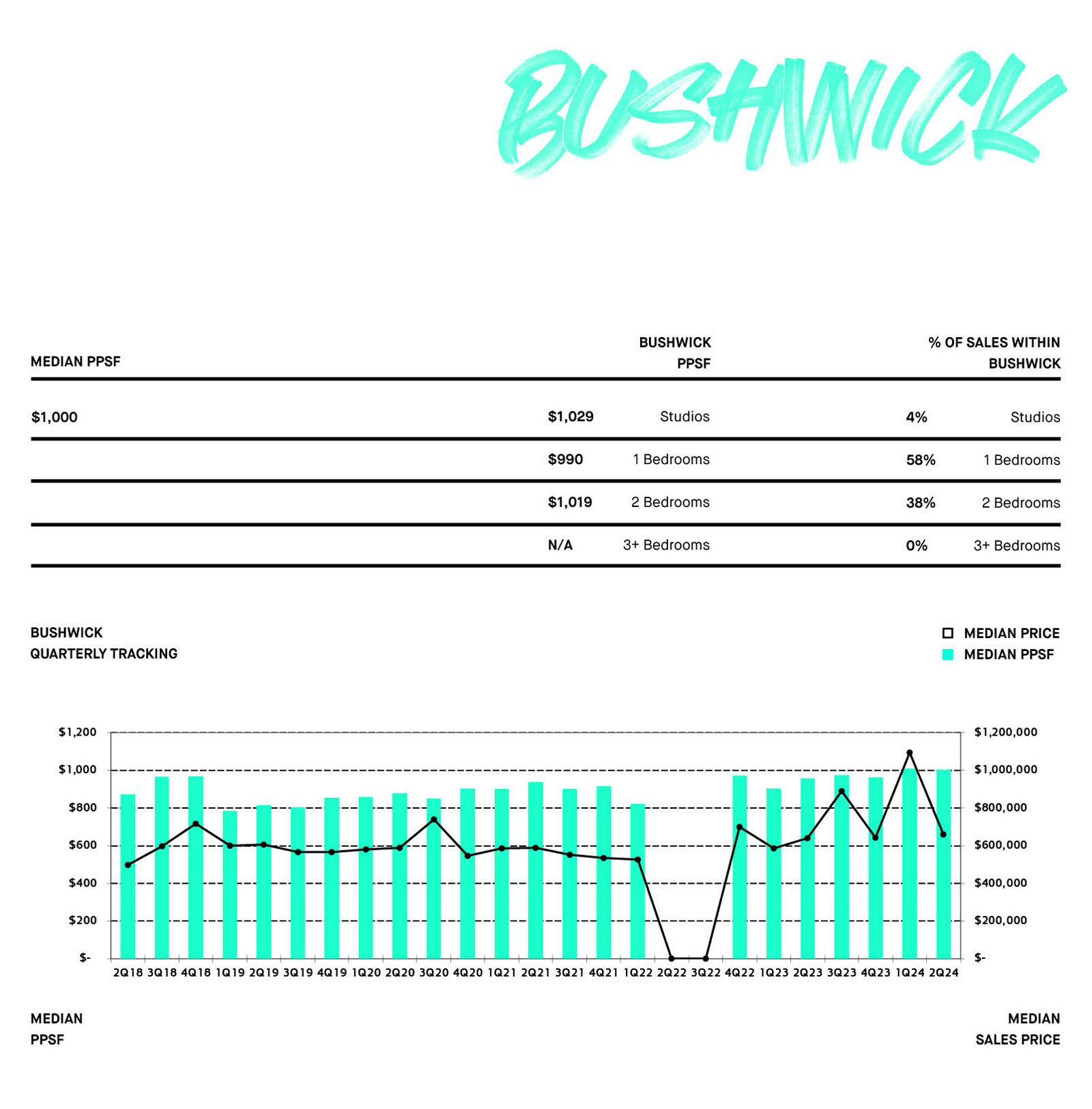

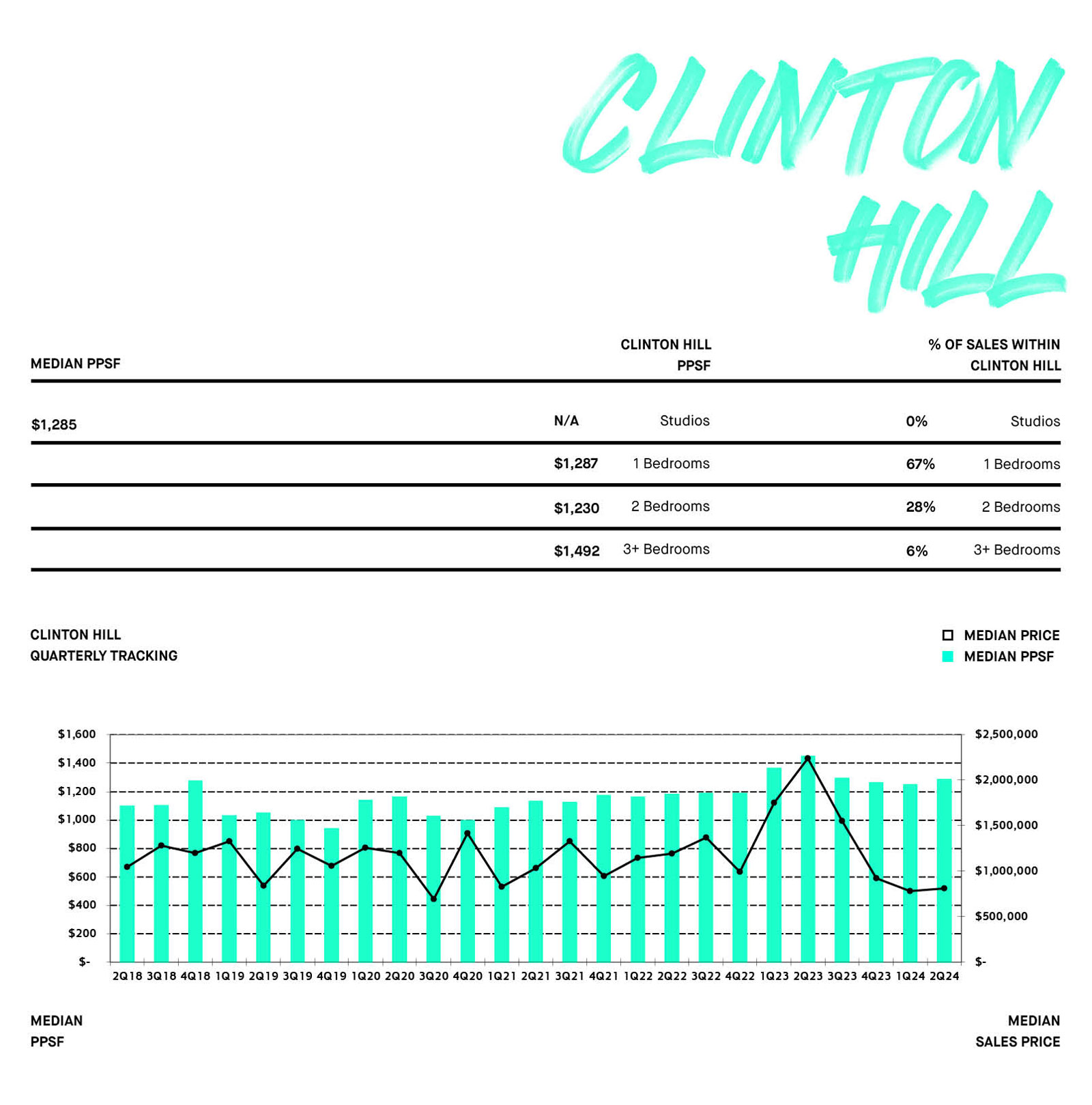

During the second quarter of 2024, there were 18 studio units that closed, representing 4.68% of the 385 total sponsor unit sales in Brooklyn, 127 were one-bedrooms (32.99%), 148 were two-bedrooms (38.44%) and 92 were three-bedrooms+ (23.90%).

NEIGHBORHOODS WHERE THE MAJORITY OF EACH UNIT TYPE WAS SOLD IN 2Q24

56%

STUDIO

GREENPOINT

29%

ONE-BEDROOM

GREENPOINT

21%

TWO-BEDROOM

GREENPOINT

24%

THREE-BEDROOM+

GREENPOINT

MARKET SNAPSHOT

2Q24 MEDIAN PRICE PER SQUARE FOOT (PPSF) BY NEIGHBORHOOD

2Q24 MEDIAN SALES PRICE BY NEIGHBORHOOD

2Q24 % OF TOTAL SPONSOR SALES BOROUGH-WIDE

NUMBER OF UNITS SOLD IN 2Q24

THE REPORT EXPLAINED

INCLUDED IN THIS RESEARCH ARE WALK-UP AND ELEVATOR NEW DEVELOPMENT CONDOMINIUM BUILDINGS, AS WELL AS NEW CONVERSION CONDOMINIUMS IF THE SALES WERE APPLICABLE SPONSOR TRANSACTIONS. EXCLUDED FROM THE REPORT ARE ALL COOPERATIVE SALES.

Unit types such as studios, one-bedrooms, and two-bedroom units are grouped by square footage ranges. Typically, studios are under 550 square feet, one-bedrooms range from 500-750 square feet, two-bedrooms from 800-1,000 square feet and three-bedrooms+ from 950 square feet to in excess of 1,500 square feet. Presented with a quarter-over quarter and year-over-year comparison, both city-wide and by neighborhood, MNS New Development ReportTM tracks the market trends throughout Brooklyn and Brooklyn. MNS offers a unique insight into the new development market by tracking stalled construction sites on a quarterly basis, a great indicator of where development in general is moving. MNS is your source to find neighborhood price per square foot analysis, average sale prices, unit type sales trends, overall price movement, neighborhood inventory comparisons, and absorption rates.

Can’t find what you’re looking for? Ask MNS for more information at www.mns.com

Contact Us Now: 718.222.0211

Note: All market data is collected and compiled by MNS’ marketing department. The information presented here is intended for instructive purposes only and has been gathered from sources deemed reliable, though it may be subject to errors, omissions, changes or withdrawal without notice.

If you would like to republish this report on the web, please be sure to source it as the “Brooklyn New Development Report” with a link back to its original location